More Filings, Better Signal? What HFIAA Means for Insider Intelligence

The Holding Foreign Insiders Accountable Act brings foreign private issuers into SEC Section 16 reporting on March 18 — but a last-minute exemptive order reshapes who actually files. For clients who rely on insider signals, the picture just got more complicated.

What Changed

Effective March 18, 2026, the Holding Foreign Insiders Accountable Act (HFIA Act) requires directors and officers of foreign private issuers listed on US exchanges to file SEC Forms 3, 4, and 5 — the same insider transaction reports domestic US issuers have filed for decades.

Then, on March 5, the SEC issued an exemptive order that significantly narrowed the scope. FPIs incorporated in qualifying jurisdictions — the entire EEA (including Germany, France, and the Netherlands), the UK, Canada, Switzerland, South Korea, and Chile — are conditionally exempt, provided the FPI is incorporated in one of those jurisdictions, its directors and officers are subject to a listed qualifying regulation, and their reports are made available in English within two business days.

The result: the March 18 filing wave is expected to be concentrated in non-exempt jurisdictions — Japan, Israel, China/Hong Kong, Brazil, India, Australia, and others. Insiders at companies such as Toyota, Teva Pharmaceutical, Alibaba, and Infosys are among those expected to file Forms 3 and 4 on EDGAR for the first time.

Until now, Form 144 — the notice of proposed sale of restricted or control securities — was one of the few SEC filings that surfaced insider activity at FPIs. For analysts covering these names, a Form 144 was a rare and therefore noteworthy event. The HFIA Act changes that for non-exempt issuers: Form 4 will now capture the full spectrum of transactions, making Form 144 one signal among many rather than the sole US-side data point.

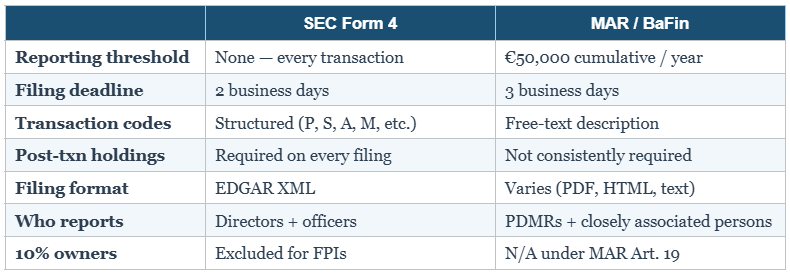

Why the Exemption — and Where the Gaps Remain

The SEC granted the exemption because it judged certain home-jurisdiction regimes to be "substantially similar" to Section 16(a). Taking the EEA's MAR framework as an example, here's how the two systems compare — and why the SEC's call was close but not obvious:

The Threshold Gap: What the Exemption Doesn't Fix

The most consequential line in that table is the first one. Form 4 has no de minimis threshold — a $500 purchase triggers the same filing as a $50 million block. MAR's baseline threshold is €20,000 cumulative per year, though national authorities can raise it to €50,000. Germany's BaFin did exactly that effective January 2026 — meaning German insiders now report even less frequently than before.

For exempt jurisdictions, this threshold gap persists. European insiders relying on the exemption will continue reporting only under MAR — meaning sub-threshold discretionary trades (below €20K in most countries, €50K in Germany) remain invisible to US investors. The exemption preserves regulatory convenience but does not close the transparency gap.

For non-exempt jurisdictions, the picture is different. A director at a Japanese issuer listed on the NYSE buying a small stake in January will now file a Form 4 within two days — structured transaction code, exact price, updated holdings. Where the home-jurisdiction regime has its own thresholds or slower timelines, Form 4 will surface trades that were previously invisible. These sub-threshold discretionary purchases are often the most interesting from a signal perspective: quiet conviction bets that threshold-based regimes filter out entirely.

Where It Gets Noisy

Dual-source duplication. For non-exempt FPIs, the HFIA Act stacks on top of home-jurisdiction reporting. The same transaction gets filed as both a Form 4 and a home-jurisdiction notification — different formats, different timelines, sometimes different dates. Without transaction-level matching, this creates phantom volume.

Compensation noise. The Form 4 feed will include a steady stream of mechanical transactions — vestings, sell-to-cover dispositions, plan exercises — that aren't conviction trades. For issuers where we previously tracked only discretionary activity, this new volume must be classified and filtered.

Exemption edge cases. The SEC's exemption applies only to officers and directors who are required to report under a qualifying regulation. If an FPI incorporated in a qualifying jurisdiction has officers who meet Rule 16a-1(f)'s definition but don't qualify as PDMRs under MAR or UK MAR, those individuals must still file Form 4. This means even "exempt" issuers may have a partial Form 4 filing obligation — a subtlety that's easy to miss.

Public filings already show this in action. Days before the March 18 effective date, a UK-incorporated FPI produced SEC Form 3 filings from multiple directors and senior officers — underscoring that an "exempt jurisdiction" does not necessarily mean "no filings." One possible explanation is that some individuals may qualify as "officers" under Rule 16a-1(f) while falling outside UK MAR's PDMR scope. Another is that the company filed on a precautionary basis while the scope of the new regime was still being assessed. Either way, data providers should expect SEC Section 16 filings even from issuers incorporated in qualifying jurisdictions.

Our Take

At 2IQ, we process multi-jurisdictional insider filings — SEC, MAR, SEDI, EDINET — every day. The exemptive order narrows the immediate Form 4 impact, but it doesn't simplify the data landscape. For exempt jurisdictions, we continue to rely on home-jurisdiction filings with their existing limitations. For non-exempt jurisdictions, we gain structured SEC data but must solve the dual-source matching challenge. And for the edge cases in between — exempt issuers with partially covered officers — we need to track both. The intelligence layer that classifies, deduplicates, and contextualises insider filings matters more now, not less.

One practical note: on March 12, the SEC staff provided limited no-action relief for FPI directors and officers who submitted their Form ID applications before March 18 but have not yet received EDGAR access. Those filers have until April 1, 2026 to file, subject to conditions. Expect some Form 3 filings to trickle in over the first two weeks rather than all landing on day one.